Weak Financing Support

High product-side risks compel third-party financiers to avoid lending in the residential rooftop solar segment. Rooftop solar solutions are viewed as ‘high-risk’ because the quality of rooftop solar products and the delivery of allied services are under the purview of the installer.

Further, the lack of standardisation of loans for residential rooftop solar solutions is another critical barrier to the growth of the residential market. Due to the relatively smaller scale of residential solar projects, banks or other financial institutions (FIs) are generally reluctant to finance them. Since there are very few cases of third-party financing for this segment, there is limited relevant data available to financiers.

Financiers are also generally reluctant to disburse loans to this market due to the poor resale value for rooftop solar systems.

Lack of Standardised and Digitised Information

Most consumers and financiers alike are not well-versed with a number of the technical terms relevant to the residential rooftop solar market. A lack of simplified information communicated between installers, financiers and consumers can delay the buying process.

Further, unlike other product classes, such as consumer durables, the residential rooftop solar market has a huge dearth of publicly accessible digital platforms with all the necessary information about various offerings for residential consumers.

Thus, the lack of digitalised experience for consumers inhibits the adoption rate of residential rooftop solar systems. The central government launched the national portal for rooftop solar installation in July 2022. It can help alleviate some of these challenges by providing a common digital platform for all related activities like system installation, vendor selection, subsidy disbursal status etc.

Keeping these challenges in mind, it is important to delve into some successful residential rooftop solar development cases. Some (if not all) of the key measures/actions taken in these cases to boost solar adoption may help alleviate the impact of the residential market’s challenges.

Success Stories

Rooftop solar development in Gujarat is undoubtedly the most successful in the Indian residential segment. Naturally, considering the domestic (Indian) market, the landmark Gujarat model needs to be studied. In this section, we provide a case study that examines the implementation strategy in Gujarat’s residential rooftop solar scheme.

Another success story that has intrigued renewable energy stakeholders globally is the solarisation drive in California, the US. California is one of the oldest solar markets in the world. This section also provides a case study that explores the current status of its robust residential rooftop solar segment.

These two case studies show two different markets making remarkable progress in terms of rooftop solar adoption. For India to achieve a similar adoption rate, the domestic market needs to evolve much more.

SURYA – Gujarat: An Exemplary Indian Solar Story

Background

In 2010, the government apportioned the NSM’s target of 100GW capacity by 2022 to all states and UTs. Gujarat had a target of 8,024MW of solar capacity, of which 3,200MW was from the rooftop solar segment.

In August 2019, the state government introduced a subsidy scheme for installing solar rooftop systems called the SURYA Gujarat (Surya Urja Rooftop Yojana Gujarat) scheme, developed exclusively for the residential category. The scheme’s target was to install 1,600MW of solar rooftop systems, covering rooftops of 800,000 households by FY2022.

While Gujarat Urja Vikas Nigam Limited (GUVNL) is the nodal agency for the SURYA- Gujarat, the state’s DISCOMs implement the scheme and disburse the subsidy.

Gujarat’s residential rooftop solar segment grew from 85MW in FY2019 to 1,227MW in FY2022. Though the state only achieved 77% of the target capacity, the residential market of Gujarat achieved an impressive CAGR of 143% between FY2019 and FY2022.

Strategy: The Gujarat government followed four essential steps to achieve large-scale deployment of residential rooftop solar in the state.

Step 1: Ensure adequate supply (building a large base of empanelled EPC contractors)

The state DISCOMs empanelled vendors as “preferred vendors” for residential consumers. A consumer seeking the rooftop solar subsidy could select a vendor only out of the list of empanelled vendors, and by FY2022, the list had more than 600 vendors. For installations during FY2023, about 1000 vendors have been empanelled.

Step 2: Ensure adequate demand (Executing consumer awareness initiatives)

The government used the following channels to disseminate relevant information:

SMS: Messages were broadcasted to 20 million residential consumers Radio spots and advertisements Advertisements on news channels and in cinema

Banners displayed at various government offices

Flyer distributed with residential consumers’ electricity bills Door-to-door public awareness programmes were arranged. Similar programmes were arranged at the Town Hall, the Nagar Palika and the municipal corporation Newspaper advertisements

Hoardings Messaging through an AI-based WhatsApp chatbot Social media communications on platforms such as Facebook, Instagram and YouTube

Step 3: End-to-end digitization (from registration to subsidy disbursement)

The state government created a unified single-window rooftop solar portal to facilitate the hassle-free implementation of the scheme. The web portal offers auto- generated e-mail and SMS delivery systems and different types of auto-generated reports on various aspects, such as solar system design, plant performance etc. The portal also integrates with the E-urja, SAP and the chief electrical inspectorate (CEI) portals.

Step 4: Timely disbursal of subsidy

The portal also monitors subsidy disbursement. As soon as the portal 27eceives a subsidy claim, the concerned division office of a DISCOM checks the same. The portal then generates the status on the subsidy. The status is available on the portal on a daily basis.

Key Insights

- Aggregating demand through strong public outreach initiatives has significantly contributed to Gujarat’s success in residential solar development.

- The proactive participation of state government agencies, especially the DISCOMs, enhanced the market’s demand and supply aspects.

- The digitization of due processes simplified both the consumers’ and vendors’ roles, enabling transparent and streamlined transactions.

The 2020 Solar Mandate: The Case of California

California has consistently been at the forefront of adopting solar energy for many years. The Million Solar Roofs Initiative, flagged off in 2006, promoted the setting up of distributed solar systems on residences, businesses and farms. This state on the west coast of the US achieved its target of one million solar roofs in 2015, much ahead of the target year, i.e., 2019. Even afterwards, the adoption of rooftop solar installations continued in the state.

In 2018, California created a new mandate for installing solar panels in new single-family and multi-family homes up to three stories high. This is the first such mandate in the US. The mandate took effect on 1 January 2020 and has been integrated into the state’s building codes.

About the Mandate

- Solar systems on new residential projects must have adequate capacity to meet all the electricity needs annually. Builders, therefore, must estimate the electricity needs for these homes based on the climate zone and the building’s floor area.

- Existing homes do not require solar panel installation unless they are undergoing extensive renovations.

- For new residential projects, solar systems are mandatory. However, there is flexibility regarding the size of the rooftop solar system. By integrating BESS with the solar system, builders can reduce the solar system size by up to 25%.

- In addition, by incorporating energy efficiency and demand-response measures into the building design, the solar system size can be further downsized by 40% or more.

Incentives

Residential consumers in California can avail of multiple incentives (as shown in Table 6), which make adopting rooftop solar systems affordable.

Impact

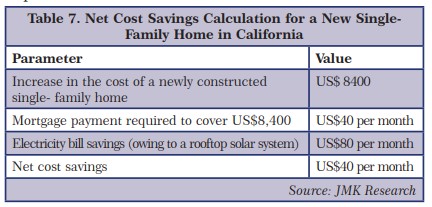

Through a cost-effectiveness study, the California Energy Commission (CEC) determined that though the upfront costs of new homes would increase, consumers would realise (estimated) savings of US$40 per month. We explain this in Table 7.

The current solar mandate in California will be updated effective 1 January 2023. As per this new mandate (known as the 2022 Energy Code), all new high-rise residential buildings must have integrated rooftop solar and battery storage systems. These new homes will need electrical wiring to transition from gas appliances to all-electric ones easily.

Key Insights

- Stringent building codes recognising rooftop solar systems as an integral component can be highly ffective in spurring the residential rooftop solar market growth.

- Offering an array of incentives, such as tax credits, rebates, cash payments, etc., is necessary to boost residential consumers’ transition to “greener’ (but higher upfront cost) new homes.

- It is also essential to incorporate forward-thinking policies and regulations and upgrade relevant (residential buildings, power transmission and distribution) infrastructure. This will enable easier adoption of upcoming mainstream technologies such as lithium-ion BESS.

Way Forward

The hunger of residential consumers for cheaper and greener power sources will drive the market in the coming years. As most residential spaces have limited space, consumer preference for high-wattage modules supported with battery storage is bound to pick momentum. Maturity in financing options in this sector will address the current financing woes. Innovative business models involving DISCOMs also look very promising regarding demand aggregation benefits.

Availability of Holistic Rooftop Solar Solutions

While an installation-plus-insurance offering exists in the residential segment in India as an adjacency, a more holistic solution is bound to create more profound value for both customers and installers/developers.

We expect embedded financing8 to become popular in the coming years. The consumer buying process can become more streamlined by bundling various business aspects, such as financing, insurance, installation, O&M, equipment supply, etc. This will certainly be a strong catalyst for solarizing residential rooftops.

Shift in Consumer Preferences Towards High-End Offerings

We expect two notable trends to become mainstream in the near term.

High-Wattage Modules

First, an increasing number of customers are opting for high-wattage solar modules along with high-quality BoS (micro-inverters, optimizers, etc.), aiming to get best-in- class rooftop solar products.

Solar-Plus-Storage

Second, in Tier 2 cities, owing to the lower reliability of the retail power supply, the purchase of hybrid solutions (solar-plus-storage) is on the rise in the residential segment. In the not-so-distant future, with falling battery costs, battery storage may become a critical component in all solar residential rooftop solar solutions.

New and Emerging Models under DISCOM-Centric Approach

The DISCOM-centric approach, as the term suggests, implies the direct facilitation by DISCOMs in developing solar systems on residential rooftops. Models under this approach are slowly emerging in the Indian context. Depending on the responsibilities of a DISCOM, there can be different models in this approach, including the DISCOM as:

- A demand aggregator

- A demand aggregator and EPC provider

-

A demand aggregator with a third-party acting as the RESCO

-

A demand aggregator and as the RESCO

Today, very few business models use the DISCOM-centric approach. However, a few states, such as Delhi, Kerala, and Andhra Pradesh, have approved or implemented examples of the different models under this approach. Additionally, a DISCOM- centric RESCO model is in the works for the residential segment in the city of Chandigarh.

…To be continued

Jyoti Gulia is the Founder of JMK Research and has about 16 years of rich experience in

the Indian renewable sector. Her core expertise includes policy and regulatory

advocacy, assessing market trends, and advising companies on their business strategy.

Akhil Thayillam is a Senior Research Associate at JMK Research. A renewable sector enthusiast, he has experience in tracking new sector trends as well as policy and regulatory developments.

Prabhakar Sharma is a Senior Research Associate at JMK Research with expertise in tracking the renewable energy and the battery storage sector. Previously, he worked

with Amplus Solar.

Vibhuti Garg is an Energy Economist and the Director, South Asia, IEEFA. She has advised

private and public sector clients on commercial and market entry strategies, investment diligence on power projects and the impact of power sector performance on state finances. She also works on international energy governance, energy transition, energy access, reallocation of fossil fuel subsidy expenditure to clean energy, energy pricing and tariff reforms.