India Ratings and Research (Ind-Ra) has maintained a stable to negative outlook on the power sector for FY18, despite an improvement in coal availability, the restructuring of discom debt and the operationalisation of stuck projects. This is owing to large underutilised capacities, muted demand, bunched capacity addition, soft merchant power prices, continued investments in renewable capacities, lack of power purchase agreements (PPAs) and weak discoms.

Moreover, Ind-Ra has maintained a Stable Outlook on most of its rated power sector entities for FY18, as the agency expects its rated entities will continue to manage fuel and state power utility risks due to a favourable tariff mechanism, a comfortable liquidity position and support from central and state governments.

Sector Consolidation Likely

Credit profiles of large-sized power companies appear to have stabilised, though the sector’s return on capital employed remains unattractive. However, small private companies are the worst hit. With a sub-50% plant load factor (PLF), they have a high probability of debt default. Under the current scenario, the survival of such players is not possible. There is a possibility of sector consolidation, which could be triggered by the new bankruptcy code.

Thermal PLF to Remain Subdued in FY18

Ind-Ra expects the PLFs of coal-based plants to decline further in FY18 and rise thereafter, though they would continue to remain sub-65% until FY22. India added nearly 115GW of coal-based capacity over FY11-9MFY17. However, demand growth did not keep pace with such capacity addition. This has put pressure on the PLFs of coal-based thermal power plants. In the past, coal and discom financial health were the two key constraints to the overall PLF. However, demand, solar capacity addition and discom financial health will be the major factors putting pressure on PLF in future.

Private Sector to be Worst Hit

Ind-Ra believes nearly 45GW of private sector coal-based capacity running at sub-50% PLF is currently stressed, with a debt of nearly INR1.9 trillion. The private sector has been hit harder due to lack of PPAs for the entire capacity. Earlier, the private sector kept a part of the capacity untied due to high short-term prices. The PLF of the private sector’s coal-based plants fell to 56.3% in 9MFY17 from 83.9% in FY10. Given short- term power prices are likely to remain benign and discoms’ unwillingness to sign PPAs, these capacities are unlikely to see an increase in PLF. Moreover, according to Central Electricity Authority (CEA) estimates, 50GW of capacity has a high probability of getting commissioned over FY18-FY22. Central and state power utilities account for 60% of the 50GW capacity, followed by the private sector (40%). PPAs have been signed for the capacity belonging to central and state power utilities. This will put further pressure on the coal-based capacity of private power generators.

Significant Headroom for Solar Prices to Fall

Solar power tariffs across the world declined to USD24MWh compared with the lowest solar power tariff of USD48MWh in India. Given the wide difference, Ind-Ra believes there is ample room for domestic solar power tariffs to fall and, more so, as prices of solar panels fell 15% in 2HFY16. Solar power tariffs globally are a function of strong counterparty, higher PLF, single axis tilt use and lower borrowing cost. Moreover, battery storage advancements worldwide could alter solar power economics and make solar a more price and consumer-friendly energy source.

Discom Turnaround Now Dependent on ATC Loss Reduction

Ujwal DISCOM Assurance Yojana (UDAY), which covers 92% of discom debt and INR 1,830.84 billion of debt issued, has been successful on the financial front. 21 states have signed UDAY. Ind-Ra believes UDAY’s future success would depend on the successful operational turnaround at the discom level, primarily through ATC loss reduction and power purchase cost management. Electricity meter manufacturers are likely to significantly benefit from the ATC loss reduction drive, as the government looks at moving towards smart meters.

Outlook Sensitivities

Sovereign Linkages, High Capex and Low Prices

Weakening of linkages of public sector enterprises with the government of India (GOI), debt- funded capex with low incremental profitability due to lower PLF and average realisations could have a negative impact on ratings.

Sector Consolidation Likely

The credit profiles of the top nine power sector entities engaged in coal-based power generation based on installed capacity seem to have stabilised. Their interest coverage stabilised at 2.4x in FY16 (FY15: 2.3x) (Figure 1) and net leverage improved to 5.3x (FY15: 6x) (Figure 2), driven by, according to Ind-Ra, the ability of these entities to enter into PPAs, thus ensuring project completion and commissioning.

Figure 1: Interest Coverage Levels of Top Nine Listed Thermal Power Sector Players

Figure 2: Net Leverage Levels of Top Nine Listed Thermal Power Sector Players

However, Ind-Ra notes that debt stress levels across power generators other than these top nine entities are quite significant. The reason behind this is that these entities have not been able to enter into PPAs or have not been able to achieve commercial operations for their capacity, leading to challenges with regard to debt servicing. Ind-Ra expects these relatively small capacities in the power generation value chain to be bought out by financial or strategic investors, thus leading to sector consolidation.

Ind-Ra expects acquirers to express interest only in lower asset valuations, with haircuts to be taken by bank and original promoters. This would be the case as acquirers would expect to generate return on equity (RoE) from assets. Given signing PPAs with discoms would be challenging, a buyer is likely to generate higher RoE from lower price paid for an asset than operational improvement expected. Mathematically, of the three levers available in RoE (i.e. profitability, asset turnover and leverage), the acquirer will derive maximum RoE through increased asset turnover reflected in lower purchase consideration for the asset.

The current power market is conducive for acquirers on account of significant stressed capacity levels. In addition, the ability of acquirers to purchase assets at higher valuations is limited due to their own leverage levels.

Capacity Sufficient; Demand Deficient; PLF to Remain Stressed

Ind-Ra expects India to remain a capacity sufficient country at least until FY22, driven by a low PLF (9MFY17: 60%) of existing coal-based capacity (185GW at FYE16), a high probability of 50GW thermal capacity addition during FY18-FY22 and an increase in power generation from renewable sources, particularly, solar. Therefore, Ind-Ra estimates India’s thermal capacity to reach 250GW by FY22. Solar, wind and hydro capacities are likely to reach 40GW, 50GW and 56GW, respectively, assuming 6GW, 4GW, 2.4GW of capacity addition each year over FY18-FY22, respectively.

However, in its base case, Ind-Ra projects 7% demand growth. The agency believes the PLF levels could start rising after FY18; however, they are likely to remain sub-65% over FY18- FY22 (higher than the current level of 60%).

However, thermal PLF is sensitive to two key variables: solar power capacity addition and demand growth. Ind-Ra’s sensitivity analysis indicates that even in the most optimistic scenario of 8% demand growth and 12GW of solar capacity addition annually, PLF is unlikely to reach the historic level of 78.6%, both on average over FY18-FY22 (Figure 3) and on an annual basis in FY22 (Figure 4).

Figure 3: National Coal-Based PL

Figure 4: Average PLF over FY18-FY22

PPA Deficient; Price Insufficient; Private Sector Worst Hit

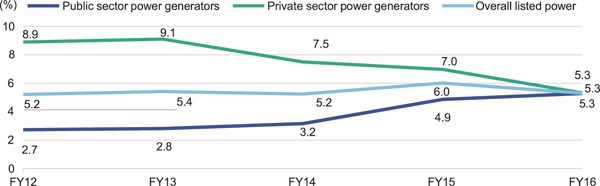

Although domestic coal supply significantly improved in the last 2.5 years, thermal power plants still continue to face related challenges. Private sector thermal plants are the worst hit, indicated by a PLF decline to 56.3% in 9MFY17 from 83.9% in FY10 (Figure 5). The decline is due to higher private sector capacity share in incremental capacity addition (Figure 6) during the period, lack of PPAs for the entire capacity and willingness to keep capacity open owing to high short-term prices prevalent earlier. Given the lack of PPAs, private thermal power plants access the merchant market for the sale of power.

Figure 5: FY22 Year-End PLF Estimates

Figure 6: PLFs of Central and Private Coal-Based Power Plants

However, as prices of power on the power exchange have fallen and are unlikely to increase in FY18, profitability from merchant sales is likely to remain low in view of a rise in imported coal prices. In addition, the possibility of a PLF improvement looks bleak. Moreover, discoms are unwilling to sign long-term PPAs and are more comfortable procuring power through the short- and medium-term PPAs, thus, putting pressure on PLF. Ind-Ra estimates stressed private sector-based thermal coal assets at nearly 45GW, which is running at sub-50% PLF. Investment and stressed debt levels are estimated at INR2.7 trillion and INR1.9 trillion, respectively.

New Capacity to Further Stress Existing Private Capacity

As of 9MFY17, the private sector operated coal-based capacity totalling 83GW was running at a 56.3% PLF. Nearly 50GW of incremental capacity is likely to be added over FY18-FY22, with nearly 60% of the capacity likely to be added by central and state utilities. Given PPAs have already been signed for this 60% capacity, Ind-Ra expects the private sector’s overall coal- based PLF to get further stressed. This is because the private sector’s upcoming capacities would find it extremely difficult to be absorbed owing to lack of PPAs for the full capacity and lack of fuel linkages. Therefore, the overall PLF of private sector coal-based plants would remain lower, leading to support requirements. However, the ability of the promoters of private sector thermal plants to infuse equity for completion and at a later stage after project commissioning is questionable, as their balance sheets are already significantly leveraged owing to minimal returns from existing plants.

Global Lowest Solar Tariff 50% Lower Compared with Domestic Lowest Solar Tariff

In September 2016, a low price for energy from solar panels (USD24MWh) was bid for a 350MW solar plant in Abu Dhabi, UAE. Meanwhile, the lowest solar power tariff in India was a USD48MWh bid in February 2017, indicating a significant 50% room for fall in prices in the country. The difference between the global and domestic solar power tariffs is extremely high; however, global solar power tariffs have been driven by strong counterparty, higher PLF, single axis tilt use and lower borrowing cost.

Figure 7: Incremental Capacity Addition by Central/State/Private Utilities

Figure 8: Levelised PPA Prices in US and Other Recent Low Tariff Bids

Ind-Ra expects domestic solar power prices to continue declining in FY18 in line with global trends. The decline would be driven by a continual fall in solar module prices and the entry of new players in the solar inverter and racking markets, with aggressive pricing leading to a decline in the balance of plants cost. In 2HFY16, global solar module prices declined 15% yoy. The decline would also be supported in future by a decline in cost of funds, access to capital markets and a reduction in equity risk premium.

However, in India, the counterparty risk continues to remain the biggest challenge due to deferred payments from discoms. If the GOI can involve a strong counterparty such as Solar Energy Corporation of India Ltd. for routing payments, risk premium building by bidders for delayed payments could be reduced.

Figure 10: Thermal Net Capacity Addition and Decommissioning

Globally, there is a high focus on making energy storage a viable option in terms of cost, efficiency and charge cycles. If successful, solar energy adoption will accelerate at a higher rate and could lead to the disruption of peaking plants. The disruption would also spread to base load plants; however, it is likely to be gradual. Once battery storage is successful, grid reliability concerns would be addressed.

Success of UDAY Depends on Operational Turnaround

The GOI has largely achieved financial book cleaning through UDAY, given 21 states are participating in the scheme. These 21 states represent about 92% of the overall discom debt. In FY16, states issued UDAY bonds totalling INR989.60 billion. Until date, UDAY bonds worth INR1,830.84 billion have been issued. UDAY bonds worth INR2,651.35 billion are yet to be issued.

The operational turnaround of discoms is pending. This could be achieved through a reduction in ATC losses. A reduction in ATC losses is possible. In Manipur, billing and collection efficiencies improved to 100% each from 63% and 64%, respectively, after the installation of 11,000 single-phase and 1,000 three-phase prepaid electric meters.

Undertaking such measures across all states under UDAY could pose a challenge owing to large capex requirements, notes Ind-Ra. However, benefits of such measures are tangible and could address the challenge of the operational turnaround of discoms. Ind-Ra has maintained a Stable Outlook on most of its rated power sector entities for FY18, as the agency expects its rated entities will continue to manage fuel and state power utility risks due to a favourable tariff mechanism, a comfortable liquidity position and support from central and state governments.

If you want to share thoughts or feedback then please leave a comment below.