Distributed Energy Resource systems (DER) are increasingly playing an important role in modern electric power distribution system. They refer to small grid connected decentralized energy generators that typically use renewable energy sources such as biomass, solar and wind power. In sharp contrast to the conventional centralized coal-fired, hydro or nuclear power plants, DER systems are located close to the load and use modular, flexible technologies. DER exploits small size for lower cost (it is now possible to mass produce small systems), reduced T&D losses (due to local generation / less site specific), low pollution, lower maintenance, lesser complexity and cost of regulatory oversight, tariff administration and metering and billing.

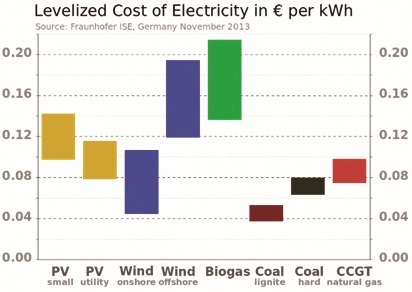

Since 2013 most of the DER systems have reached grid parity – a point at which the DER can generate electricity at a Levelized Cost of Electricity (LCOE) that is less than or equal to the end consumer’s retail price (see Figure 1). Reaching grid parity is essential for an energy source to be a contender for widespread development without subsidies or government support.

Figure 1. Levelized Cost of Electricity for DERs

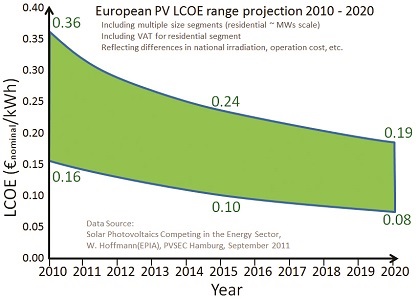

Solar photovoltaic (PV) and wind (see Table 1) reached grid parity even earlier (in 2010), and this has been a catalyst for growth of these two DER systems in a number of markets such as Europe, Australia, and US. Figure 2 shows the drop in LCOE for solar PV for the European markets.

Figure 2. Drop in LCOE for Solar Photovoltaics

Since grid parity dictates the success of DER systems, it is clear that the associated tariff policies, tariff mechanisms, compensation and purchase arrangements play a vital role in sending clear signals to the public for their involvement. There are three compensation mechanisms that are designed to accelerate investments in DER systems:

1. Power Purchase Agreement (PPA), also known as the ‘Standard Offer Program’ offers compensation that is generally below retail. It could be above retail, particularly, in case of solar where generation is close to peak demand.

2. Feed-in Tariff (FiT) which is usually set initially above retail and reduces down to retail as the percentage of DER adopters increase.

3. Net Energy Metering (NM) which is always at retail. Since the DER is mostly used for own consumption, technically, it cannot be termed as compensation, although it may be considered so if there is excess generation and if utility is allowed to make payments for the same.

In this paper, we will take a close look at each of the three tariff mechanisms and understand their pros and cons, in particular, for solar PV. We also consider the experiences of some of the countries where implemented, so that we can pick one that is best suited for our country.

Compensation Mechanisms

Power Purchase Agreement (PPA) based System

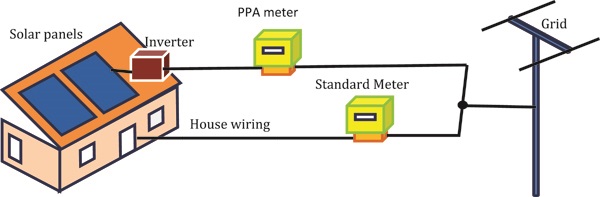

Onsite renewable Power Purchase Agreement (PPA) allow agencies to fund PV projects with no up-front capital costs incurred. With the PPA, a developer installs a PV on agency property under an agreement that the agency will purchase the power generated by the system. The agency pays for the system through these power payments for the life of the contract, while the developer installs, owns, operates, and maintains the PV system over the same contract life.

Under the PPA mechanism, the energy generated and the consumed by the agency / consumer are metered separately using two meters, namely, the PPA meter and the standard consumer meter respectively (see Figure 3). Due to this independence, under the PPA, neither the agency who pays for the power generated by the PV system, nor the developer who owns and operates the PV system, need to be a consumer of electricity. The PPA solely binds the agency and the developer, and therefore, is outside the scope, jurisdiction, and purview of the Electric Regulatory Commissions (ERCs). An exception to this is when the agency happens to be a local electric utility, in which case the tariffs would be under the purview of the ERCs.

Figure 3: Parallel Connected Power Purchase Agreement (PPA) Meter

PPAs feature a variety of benefits and considerations for utilities or government agencies.

Benefits to the utility/ agency

• No up-front capital costs

• Typically, a known, long-term energy price

• Ability to monetize tax incentives

• No operations and maintenance responsibilities

• Minimal risk

Considerations:

• Utility/ government sector experience with PPAs is in its infancy/ still growing

• Challenges and concerns with site access contracts

• Contract term limitations

• Inherent transaction costs

However, as of 2009, many of the electric utilities have stopped accepting new PPA applications. For example in Ontario, Canada, the Renewable Energy Standard Offer Program (RESOP) has been replaced by the Feed-in Tariff (FiT) program.

The PPAs are individual contracts and are of lower significance in our current context. Hence, we will proceed to evaluate the remaining two, more interesting, compensation mechanisms.

Feed-in Tariff (FiT) System

Feed-in Tariff (FiT) schemes are typically based on a 15 – 20 year long contract where prices are pre-defined above retail with a tariff degression, which effectively reduces the earnings over time. In the FiT, you get paid for every kWh you generate under anFiT contract.

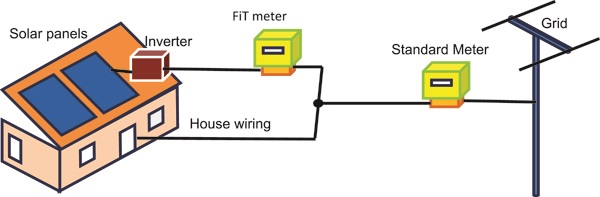

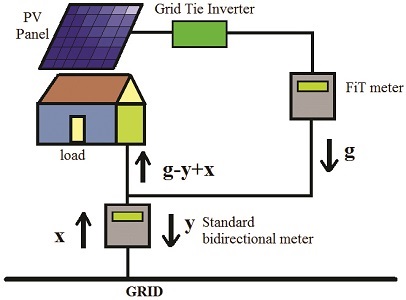

The FiT system uses a separate meter called a FiT meter (see Figure 4) in order to measure the outflow of electricity generated from renewable energy on the consumer’s premises independently. The FiT meter is usually uni-directional, but if we are interested in knowing the consumption of small (usually insignificant) amounts of power by the PVs when they are themselves not generating, then we could consider it to be a bi-directional meter.

The electricity consumption is measured by the standard meter which is compulsorily a bi-directional meter (see Figure 4). The separation of electricity generation and consumption using two meters enables each to be priced separately.

Unlike the meter connections under the PPA scheme, in case of the FiT, it is possible to identify how much kWh units consumed by the consumer has been generated by his own PV system at any particular instant of time. Since only the surplus energy generated by the PV at any instant of time gets exported through the standard meter, it is possible to have a tariff rate applied to the surplus energy that is different from the rate applied to the total energy generated by the PV system.

The FiT systems are popular for solar generation in several European countries including Germany. In order to boost solar power, German utilities once paid several times the retail rate for solar, but has successfully reduced the rates drastically while actual installation of solar has grown exponentially at the same time due to installed cost reductions. Since the German system pays what each source costs with a reasonable profit margin, wind energy, in sharp contrast, only receives around a half of the domestic retail rate. As a result of these measures, Germany has the highest PV installed capacity of 39 GW (as on 2015) of which 71% is in the rooftop segment. The PV Watt per Capita is also the highest in Germany at 491 (whereas it is only 4 in India).

However, long term contracts could have its risks. Malta is in the news, with a finding by its energy minister of irregularities in a €35 million FiT contract for the installation of photovoltaic panels on public buildings that binds the country for 35 years. While the contract provided a feed-in tariff of 23 cents per kWh for 25 years, it should actually have been 16 cents.

Figure 4: Series Connected Feed-in-Tariff (FiT) Meter Connections

Net Metering

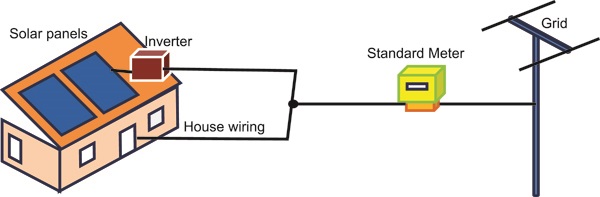

Net Energy Metering or simply Net Metering (NM) is a service offered by the local electric utility to an electric consumer under which electric energy generated by that consumer and delivered to the local distribution grid may be used to offset the electric energy provided by the electric utility to that consumer during the applicable billing period. Unlike FiT, the NM requires just a single bidirectional energy meter (see Figure 5).

Though the NM policy is designed to foster private investment in the renewable energy, it varies significantly by country and by state: if NM is available, if and how long you can keep your banked credits, and how much the credits are worth in retail or wholesale. In general, the NM policy involve a monthly roll over of energy (kWh) credits, a small monthly connection fee, monthly payment of the deficits which is the normal electric bill, and annual settlement of any residual credit.

In USA, net metering is popular in 43 States. The US Energy Policy Act 2005 mandates all public electric utilities to make net metering options available to all the customers. California has over 1 lakh net metering consumers with maximum solar capacity of 991 MWp. The NM policies are far more popular than the FiT policies in the US and in Japan.

Figure 5: Net Energy Metering (NM) Meter Connections

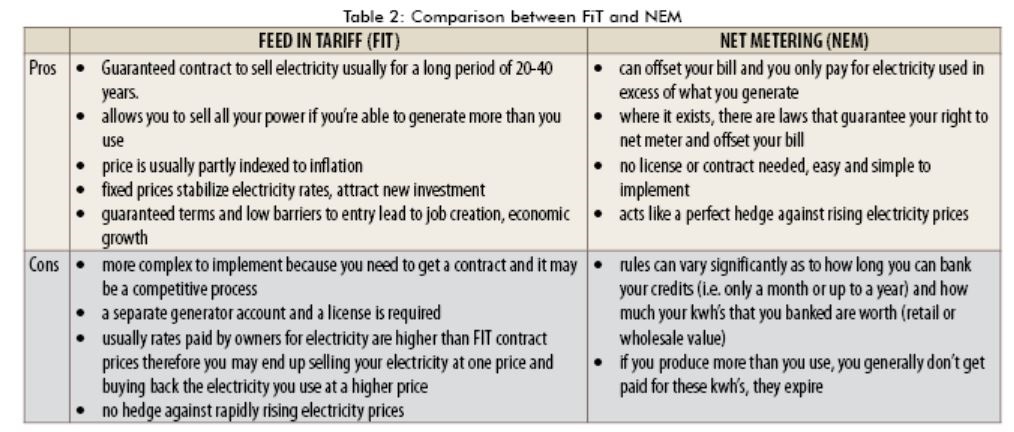

Comparison between FiT and NM Mechanisms

Table 2 highlights some of the differences between FiT and NM, their pros and cons.

Advantages of NM

We believe that any Indian consumer who is interested in generating energy using renewable means should be allowed to do so; moreover, encouraged to do so. NM needs no license. NM is about respecting and protecting the rights of individual home owners to generate their own power for their own use particularly from a renewable resource. This leads one to believe that NM is the most appropriate mechanism for a democratic country like India. However, we do not consider so due to the severe limitations that a single meter topology offers – this gets clarified in the following sections.

Instead of wasting the excess electricity, under NM it is provided to the local distributor who will apply the credits for that excess towards the electricity bills. Grid-access has been the point of contention for NM. Electric utilities argue that under NM one may use an isolated PV to generate but not with a grid connection. To this, the counter argument would be – electricity is a perishable commodity that cannot be stored efficiently. It is in the best environmental interest to feed excess energy generated by PVs into the grid, and hence, local electric utilities should facilitate the same.

Advantages of FiT

Since NM protects the rights of consumers, it does not mean that the FiT model has no role to play. Two decades back, Western Europe’s landmark FITs were tremendously important in jump starting the solar industry. FITs work well in places where the cost of retail electricity is low and the cost of electricity from solar systems is high. FiTs are also far more stable since they are contracts with a binding term on both parties. But today we have outgrown those infant days when one needs to deliberately over-pay to get solar built. Today, some say that there is contraction in the German market, turmoil in other European countries and in some states of US. The first and most famous US FiT – the Gainesville Regional Utilities program started in 2009 has been suspended in 2014. Over five years the utility has paid $11.4 million at a solar generated electricity price of 0.29 cents per kWh. To account for this FiT, residential rates were raised by 0.3 cents per kWh. But, due to FiT, Gainesville has reached its solar targets. It is to be seen if Gainesville will be setting new targets for the forthcoming years, and if so, the model it would choose.

Though US favours NM, its residential consumers are not the major beneficiaries. Electric utilities also complain that NM takes the revenues away from the utilities base. A close study will reveal that it is solar leasing companies that derive their fees and maximum profit from NM. The utilities and consumers sell their rights to a leasing company to develop solar power.

On the other hand, community banks and credit unions prefer FiTs as they are more bankable. With a FiT, a community can take a loan from a bank and install renewable energy project on their own.

Germany has been the most successful with FiT after restructuring the Feed-in Law as the ‘German Renewable Energy Act’ in 2000. This Act has proved to be the world’s most effective policy framework at accelerating renewable deployment. The German FiT policy (amended in 2004 and 2008) brought in important changes:

1. Purchase prices were based on generation cost. This led to different prices for wind power, solar power, biomass/biogas and geothermal and for projects of different sizes.

2. Purchase guarantees were extended to 20 years.

3. Utilities were allowed to participate.

4. Rates were designed to decline annually based on expected cost reductions, known as “tariff degression”.

Under FiT, long-term contracts were offered in a non-discriminatory manner to all renewable energy producers. Purchase prices were based on costs. FiT policies typically target a 5–10% return. Efficiently operated projects yielded a reasonable rate of return. FiT resulted in growth of solar power in Spain, Germany, Ontario (Canada) while that of wind power in Denmark.

The success of photovoltaics in Germany resulted in an electricity price drop of up to 40% during peak output times. It resulted in savings between €520 million and 840 million for consumers. It also had a positive impact on job creation and economic growth.

However, savings for consumers have meant conversely reductions in the profit margin of the big electric power supply companies. Increase in the solar energy share in Germany also had the effect of closing gas- and coal-fired generation plants. The big electric power supply companies reacted by lobbying the German government, which reduced subsidies in 2012. Electric utilities also lobbied for the abolition, or against the introduction, of feed-in tariffs in other parts of the world, including Australia and California.

This leads one to believe that the NM suits residential scale PVs of capacities upto 100 kW, while the FiT is unparalleled at unleashing the commercial and community scale segments with larger PVs having capacities more than 100 kW.

Regulatory Framework in Gujarat

Let us now change focus to India and, in particular, to the State of Gujarat. The policies that has been put in place to accelerate the growth of renewable energy in the energy mix are:

1. The National Action Plan on Climate Change (NAPCC) launched by the Government of India in June 2008 – a comprehensive plan that targets an increase in renewable energy purchase by 1% a year with a target to achieve 15% renewable by 2020.

2. Gujarat’s Solar Power Policy-2015, launched on 13th August 2015, after the earlier policy (2009) resulted in a cumulative solar capacity in excess of 1000 MW.

3. The Jawaharlal Nehru National Solar Mission (JNNSM) launched in January 2010 that targets 22 GW of net installed solar generating capacity throughout India by 2022.

To achieve the targets put forth in the Gujarat’s Solar Power Policy:

1. Gujarat ERC (GERC) passed its Solar Tariff Order No 3 of 2015, determining a levelized tariff for kilowatt scale power plant, for the period from 1st April 2016 to 31st March 2017, at `7.83 per kWh (without accelerated depreciation benefit) and at `7.11 per kWh (with accelerated depreciation benefit).

2. During the same period, GERC has determined a levelized tariff for large Megawatt scale power plant, at `6.30 per kWh (without accelerated depreciation benefit) and at `5.74 per kWh (with accelerated depreciation benefit).

3. GERC has further mandated a specific solar Renewable Purchase Obligation (RPO) at 1.75% for 2016-17. This represents the minimum quantum of purchase from solar for each distribution licensee and other captive and open access users consuming electricity generated from conventional captive plants in Gujarat.

4. GERC has been regularly initiating Suo-Motu proceedings to verify the RPO compliance each year with Gujarat Energy Development Agency (GEDA), a nodal agency for monitoring of RPO in the State of Gujarat, as a party

5. CEA has notified “Technical Standards for Connectivity of the Distributed Generation Resources-CEA Regulations 2013” in October 2013 which permits the grid connectivity of SPV rooftop also.

6. Ministry of Power approved CEA’s draft – Installation and Operation of Meters- Regulation 2013” for metering arrangement for inter connection of SPV rooftop with grid.

7. CERC has brought out the draft guidelines for grid connectivity and metering arrangements for SPV rooftops.

8. MNRE has included Grid connected SPV rooftops in the “off grid and de centralized solar applications” scheme vide amend no.5/23/2009-P&C dated 30th October 2012 for SPV plants upto 100 kW capacity.

9. MNRE subsidy upto 30% on the following benchmark cost of the projects is available : Upto 100 kWp : `100 /Wp, and for 100 to 500 kWp : `90 /Wp

10. A separate scheme on “Grid connected rooftops and small solar systems” has been formulated which is under approval.

11. Gandhinagar city initiated a 5 MW (4 MW in government buildings and 1 MW in private homes) rooftop PV programme based on FIT/sale to utility.

12. Two project developers for 2.5 MW each selected through reverse bidding with GERC cap of`12.44/kwh.

13. Torrent Power to buy from Azur @ ` 11.21/kWh for25 years and Azure will pass on `3.0/kWh to rooftop owner as roof rent.

14. Five more cities-Bhavnagar, Mehsana, Rajkot, Surat and Vadodara started installing pilot rooftop projects.

Issues Hampering Proliferation of PVs in India

In the year 2016 many Indian states are still struggling with their roof-top programs while Germany has succeeded with it two decades back. The German FiT policy has resulted in a 40% drop in the price of electricity rates at peak times, and is considered to be most effective at accelerating renewable deployment.

One of the main reasons why India has not been successful with the proliferation of solar is the discriminatory approach taken while offering contracts. In Germany, the long-term contracts were offered in a non-discriminatory manner to all the renewable energy producers on a cost plus basis with 5-10% return.

It is also important to note that all the programs initiated in India fall under the PPA category or more recently under the NM category. Though the NM policies have been implemented in US, we show below that it is not suitable for India. For the widespread proliferation of PVs in India we explain below why there is an urgent need to shift to the FiT policy and re-design the tariffs after linking them with the existing consumer tariffs.

Problems Linking with Residential Consumer Tariffs

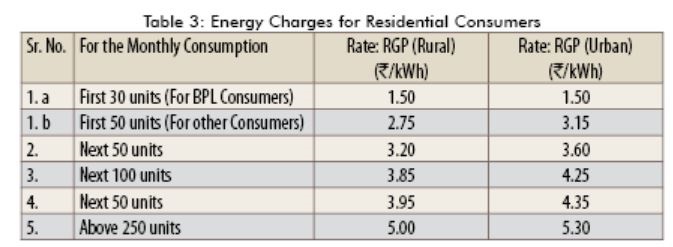

For large scale proliferation of the Solar Roof-Top projects, it is important to involve the residential consumers. To understand the impact of the current residential consumption tariff, let us take a look at one such tariff, for the year 2014-15, set as per the directives of GERC for an electric utility in Gujarat, namely, MGVCL. The tariff applicable to all residential premises located in the area serviced by MGVCL are covered under Rate : RGP (Rural) and Rate : RGP (Urban), as shown in Table 3.

It can be observed from Table 3 that the energy charges for residential consumers vary considerably as per their monthly consumption: from ` 1.50 per kWh to ` 5.30 per kWh. This is because in India, unlike developed countries, it is believed that subsidy or concessions should be offered to low consumption households. Table 3 also shows extra concessions available for consumers located in rural areas, and for consumers categorized as ‘Below the Poverty Line’ (BPL).

As we have stated earlier, it is our firm belief that those interested in generating energy using PV, should be encouraged to do so. In particular, the smaller consumers should not be discriminated with regards to benefits that accrue from solar generation. Only then can we consider the policies to be fair in a democratic regime.

Discrimination under the NM Mechanism

Since the NM mechanism has a single bidirectional energy meter it is not possible to measure the PV generation that is self-consumed. Only the surplus PV energy generated and exported to the grid is measured by the NM meter and hence purchased by the Distribution Company (DisCom) at a rate that is fixed by ERC. This rate is called the Average (pooled) Power Purchase Cost (APPC) rate, and is based on the levelized cost (LCOE) of solar energy generation (` 7.50 per kWh). As per the Gujarat Solar Power Policy-2015 and the GERC Order No. 3 of 2015, the APPC rate for the year 2016-17 for kW scale PV power plant is `7.83. This rate is much higher than the subsidized or concessional tariff rates for consumption offered to a small consumer, say ` 2.75 per kWh for a rural consumer with consumption less than 50 units – (see Table 3). It is a pity that, under the current subsidized tariff regime, small consumers with roof-top solar generation units tend to lose their existing benefits when billed under the NM mechanism.

Though the large residential consumers in urban areas lose too, they would lose less from the solar generation, in comparison, since they can offset their own more expensive consumption units (exceeding 250 units costing a higher rate of ` 5.30 per kWh). Simultaneously, these large consumers can reap an additional benefit – as they would be consuming or drawing less energy from the grid, thereby falling into the smaller consumption slabs that attract a lower tariff rate and that were originally intended for small consumers.

Regardless of the category of the residential consumer, since the cost of energy consumed (see Table 3) is lower than the APPC rate of solar generation (`7.83 per kWh), the payback period for the investment put by such consumers gets extended. This explains why residential consumers do not find solar generation attractive and why roof top solar policies have remained a miserable failure in India.

In spite of the simplicity of NM mechanism (single meter; no license requirement) making it ideal for a democratic country such as India, the disparity between APPC rate and subsidized residential tariff is powerful enough to reject this mechanism.

Figure 6: Energy recorded by FiT and standard meters

Achieving Fairness with an FiT Mechanism

An FiT tariff can be designed in a fair manner unlike an NM policy. This is because to implement FiT we have two meters from which it is possible to take four readings, namely:

g: Energy generated by the solar grid tie inverter (exported) and recorded by the FiT meter

s: Energy consumed by the solar grid tie inverter (imported) and recorded by the FiT meter

x: Energy drawn by consumer (imported) from utility grid as recorded by the Standard meter

y: Net Energy (exported) to the utility grid as recorded by the Standard meter

For all practical purposes, we may neglect the energy consumed by the solar inverter, namely, s. Even if s is significantly high, it would not make too much difference as this consumption gets accounted in the Standard consumer meter reading, x. This strategy would help reduce the number of meter readings per consumer from four to three and also reduce the cost of the FiT meter which can now be unidirectional.

Part of solar generation consumed by the consumer = (g – y)

Total energy consumed by the consumer = (g – y) + x.

For the total energy consumed, namely (g – y) + x, the same tariff as given in Table 3 is still applicable and requires no change. The only difference in the billing process, in the case of a consumer with roof-top solar generation, would be felt by the meter reader who would now need to extract three readings from two meters instead of a single one. But, in the era of smart metering, with automatic meter reading infrastructure, this cannot be viewed as a major disadvantage.

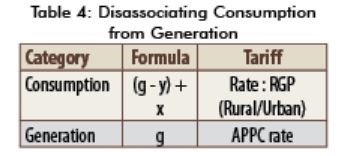

The FiT achieves fairness in the compensation mechanism by giving the ability to disassociate the consumer’s own consumption from the solar generation. Accounting is done in two stages:

a. For Consumption: The (g – y) + x formula supported under the FiT mechanism ensures that every consumer is entitled to the concessional tariff rate that is applicable to him depending on his category and consumption slab, regardless of whether he has roof top solar or not. There is no discrimination, to a consumer who is also a generator, in terms of his consumption bills.

b. For Generation: The DisCom would pay the consumer for the total number of units generated by the solar PV, namely g, recorded on the FiT meter, as per the APPC rate fixed by the ERC for that year regardless of whether these units are self-consumed or not.

The disassociation of generation from consumption under the FiT mechanism is summarized in Table 4. Thus, the above tariff scheme ensures a deterministic payback period that is independent of the consumer category and the consumption slab which was not the case under NM. Hence the implementation of the FiT policy would bring in a fair regime that will promote solar PV in the high volume, small consumption categories.

Conclusions

In, GERC has estimated the typical cost per Kw of roof top grid connected PV power plant to be `80,000. It has also considered the O&M cost of a PV power plant to be `1090/kW/annum escalating annually at 5.72%. A residential consumer would be interested in a roof top project provided he is able to recover the cost from the solar generation. The presence of subsidy in the residential consumer categories made solar generation less attractive since the payback period went up to 8-10 years. Moreover, since the subsidy differed slab wise, the payback period also differed accordingly. This explains why the solar has been a total failure in the residential roof top category and partial failure in commercial categories.

In this paper, we have not only identified the cause of failure but have also given an elegant proposal to bring in fairness in this categories. The FiT mechanism allows us to dissociate consumer’s consumption from his generation so as to allow the entire generation to attract the higher APPC rate. This shortens the payback period to 4-5 years making the roof top project attractive to the consumers. Learning from the German experiment, which has 71% generation in roof top segment, we can confidently say that a simple shift in the compensation mechanism from NM to FiT would act as a great enabler to attract even the small residential consumers, and make solar roof top an overwhelming success in India too.

If you want to share thoughts or feedback then please leave a comment below.