As far as transformation of our power sector is concerned, India has set a landmark in 2025 by achieving an unprecedented ~50% of its installed electric power generation capacity from non-fossil fuel sources. Moreover, it has happened five years ahead of its 2030 commitment under the Paris Agreement.

Our government is committed to build a sustainable world and scaling up solar capacity through initiatives like the International Solar Alliance. It is nothing but the reflection of our country’s potential to harness solar power in collaboration with more than 120 signatory countries.

However, even today, we are to some extent depending on imports of several key solar components like solar cells, wafers and polysilicon. Just for an idea, in FY 2024–25, India imported over 35.26 million solar Photovoltaic (PV) modules, valued at approximately USD 1.6 billion. Imports of total solar products (cells and modules) for the first nine months of calendar year 2025 reached approximately USD 2.9 billion. Of course, our dependence on other countries has been decreasing rapidly with our fast-growing manufacturing capability and strong government policy support.

With this backdrop, let us see today what is expected from our front-runner solar equipment manufacturers in 2026.

Expected growth in domestic solar equipment market in 2026

The domestic solar equipment market demand in 2026 is expected to see a strong and significant growth in India.

India is one of the principal growth engines for the solar market, with high demand across utility-scale, commercial, and residential sectors. Our country is forecast to add approximately 41.5 GW of new solar capacity in FY 2026, including 8 GW from rooftop systems. This growth is backed by government initiatives like the Production Linked Incentive (PLI) scheme, which is boosting domestic manufacturing capacity for modules, cells, wafers and ingots.

India’s solar manufacturing strategy for 2026

India’s solar manufacturing for 2026 is focused on massive capacity expansion, vertical integration (wafer to module), adopting advanced TOPCon/HJT tech, and enforcing local sourcing via ALMM (Approved List of Models and Manufacturers) for cells by mid-2026, driven by PLI schemes to achieve self-reliance and meet growing domestic demand, with significant growth expected in rooftop solar and export potential.

Gist of the expected key trends in 2026

- Capacity Boom: India aims for over 40 GW of solar cell capacity and 100 GW of module capacity by mid-2026, with plans to exceed 90 GW cell capacity by Q1 FY27.

- Government Push: The Production Linked Incentive (PLI) Scheme and the ALMM mandate (compulsory for cells from June 2026) are key drivers, creating guaranteed demand for domestic products.

- Advanced Technologies: A shift from basic PERC to higher-efficiency n-type TOPCon, Heterojunction (HJT), and bifacial modules is expected.

Backward Integration: Companies are investing in wafer manufacturing (e.g., Premier Energies’ JV) to reduce import dependency.

Views of a few renowned market predictors

Consolidation of players: ICRA

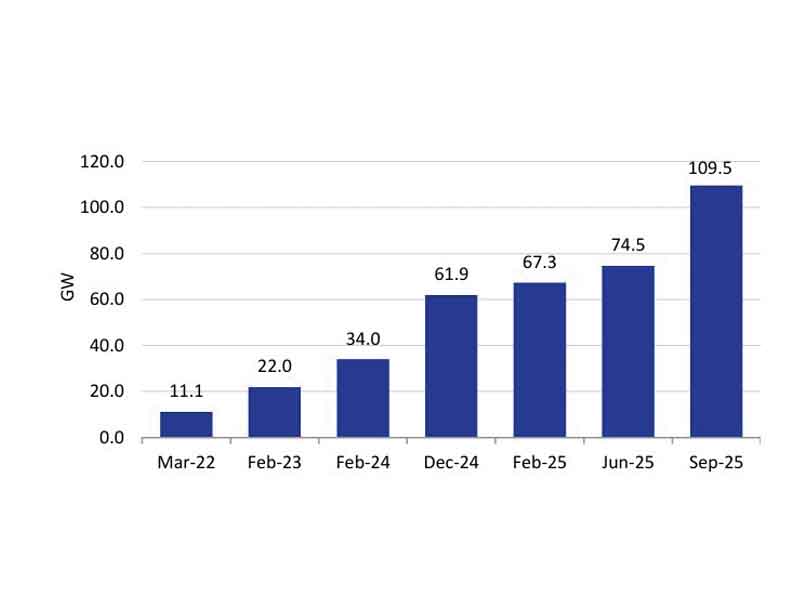

According to ICRA Ltd., the implementation of ALMM for solar PV cells from June 2026 has also fast tracked the expansion of cell manufacturing capacity in India, which is likely to increase to about 100 GW by December 2027 from 17.9 GW currently under ALMM. While this is positive for solar OEMs, the cost of domestic modules using cells from domestic OEMs is likely to exceed the cost of modules using imported cells by 3-4 cents/watt.

The annual solar module production is expected to be higher than the projected annual solar capacity installation of 45-50 GigaWatt direct current (GWdc). Further, the recent imposition of US tariffs has redirected modules from the export market to the domestic market. Hence, the overcapacity in module production will likely lead to consolidation of smaller/pureplay module players. However, the vertically integrated manufacturers will benefit over the long term due to greater control over the supply chain.

Strategic Inflection Points: TERI

India has won the module battle – but could still lose the war upstream. At ~144 GW/year, domestic module lines now far exceed annual demand (~54 GWac). However, India still imports ~90% of its wafers and nearly 100% of its polysilicon. TERI’s recent report (India’s PV Manufacturing & Its Strategic Inflection Points) warns that without new wafer slicing and large-scale polysilicon projects before 2028, upstream deficits – rather than module capacity – may constrain India’s solar ambitions.

Toolchains are emerging as the new chokepoint. Over 90% of high-end furnaces, PECVD/ALD tools, diamond-wire saws, and other critical equipment are currently imported, with limited domestic OEM presence for polysilicon and ingot lines. This exposes the sector to forex volatility, logistics disruptions, and geopolitical risk unless equipment-focused incentives and domestic R&D are accelerated.

Affordable, blended capital will determine whether upstream fabs are built. The report highlights that sovereign ‘Green-PV’ bonds, NIIF co-equity, concessional DFI debt, and risk-mitigation instruments could reduce borrowing costs to ~4–5%. This shift is essential for improving bankability and narrowing India’s cost gap with global competitors.

ESG (Environmental, Social, and Governance), circularity, and digital traceability are becoming prerequisites for export markets. With evolving compliance regimes – such as U.S. forced-labour checks, EU CBAM, and digital product-passport requirements – buyers are increasingly demanding batch-level provenance and low-carbon footprints. The findings suggest that early adoption of digital traceability tools and recycling targets can convert compliance into a competitive advantage for ‘Made-in-India’ modules.

Clusters, innovation pipelines, and skilled talent will differentiate leaders. The study recommends the development of Solar–Semicon Technology Parks, shared pilot fabs (TOPCon, HJT, tandem), and a PV–Semicon Skill Council. These initiatives aim to link PLI support to apprenticeship outcomes and a target of at least 30% women on the shop floor.

Initiatives of some prominent solar manufacturers

In 2026, Indian solar manufacturers like Waaree Energies, Adani Solar, Vikram Solar and Jakson Group are significantly ramping up production, driven by government support (PLI Scheme, ALMM) and strong demand, with plans for expanded integrated facilities (ingots, wafers, cells, modules) to boost both domestic supply and global exports, focusing on high-efficiency modules to meet rising energy needs and India’s clean energy goals. Let us see a few such targets:

- Waaree Energies: Diversifying its 6 GW integrated capacity across locations (Gujarat, Maharashtra) for ingots, wafers, cells, and modules, while also expanding energy storage manufacturing.

- Adani Solar: Aggressively scaling up its fully integrated manufacturing, producing ingots and wafers, aiming for 10 GW capacity by 2028.

- Vikram Solar: Commissioned a new 5 GW advanced facility in Tamil Nadu, increasing total capacity to 9.5 GW.

- Jakson Group: Investing heavily (`8,000 Cr) in a 6 GW integrated plant in Madhya Pradesh for major exports to US, Europe, and West Asia starting FY2027.

- Tata Power Solar: A major player with extensive experience, backed by the Tata Group, contributing to large-scale solutions.

Conclusion

It is widely expected that India will be self-sufficient in solar module manufacturing by the turn of 2026, though some reliance on imports for certain upstream components may persist.

The Indian government’s ‘Atmanirbhar Bharat’ (self-reliant India) initiative; especially, the Production Linked Incentive (PLI) scheme and the Approved List of Models and Manufacturers (ALMM); has been a primary catalyst for the exponential growth in domestic solar manufacturing capacity.

A significant step is the government’s mandate, effective June 2026, that all clean energy projects must use domestically manufactured solar cells. This is expected to drive a massive expansion in cell production to match the already high module capacity.

Key Indian corporations like Reliance Industries, Tata Power, and Adani Group are making substantial investments to establish vertically integrated manufacturing facilities, covering the entire value chain from polysilicon to modules, to meet the projected demand.

However, we will have to focus on improving a few challenging areas like: i) upstream component reliance, ii) Cost competitiveness and iii) Technology & R&D.

By P. K. Chatterjee (PK)