India’s net-zero ambition by 2070 demands deep decarbonisation of its emission-intensive sectors, which includes steel, cement, and power. Carbon Capture, Utilisation, and Storage (CCUS) has emerged as a critical bridge technology for India’s hard-to-abate sectors that can enable emission reduction while sustaining industrial growth.

India’s theoretical CO2 storage potential exceeds 600 gigatons, but deployment remains at a nascent stage. To meet the 750 Mt/year capture target by 2050, significant scaling and huge investments are required. Recently in Sept 2025, the Centre has proposed `38,900 crore (US $ 4 bn) CCUS programme with phased rolled out. Initial six years will focus on focus on carbon-intensive sectors such as power, steel, cement, chemicals, coal gasification, and green hydrogen.

A mature CCUS ecosystem must integrate all four value-chain elements: transport, utilisation and storage – where each requires distinct technology, infrastructure, and commercial frameworks. Although global models are effective, India needs a strong CCUS ecosystem with technologies that are investible, monetisable, and scalable to support a low-carbon economy.

Monetisation – The Gamechanger for CCUS

India’s Carbon Credit Trading Scheme (CCTS), launched in 2024, a rate-based ETS covering an initial nine energy-intensive industrial sectors, marks a pivotal shift. Under the framework, credit certificates will be issued to high-emitting facilities that outperforms benchmark emission intensity levels, while others must purchase them to offset excess emissions, turning carbon into a monetizable commodity. Rate-based ETSs provide options for addressing future growth uncertainty and considerations related to international competitiveness. Additionally, On March 28, 2025, India’s Ministry of Power announced the approval of eight crediting methodologies, including for renewable energy, green hydrogen production, industrial energy efficiency, and mangrove afforestation and reforestation. The gradual transition from the current market-based to these recent programs will transform carbon from a liability to an asset. Without monetisation, capture remains costly; with it, CCUS becomes an investable business.

In India’s voluntary market (2024), carbon credits trade at `200–`300 per tonne of CO2 (US $2–3/tCO2), which is quite low when compared to other developing nations – Sri Lanka (US$3.77), Bangladesh (US$4.45), and Pakistan (US$28.11), data from wood magazine. By 2026, within the compliance market, carbon prices are projected to reach `800–`1,000 per tonne (US$10–12/tCO2)). In a government-regulated system, specific industries are required to adhere to emission reduction regulations, resulting in a more structured approach to demand and pricing.

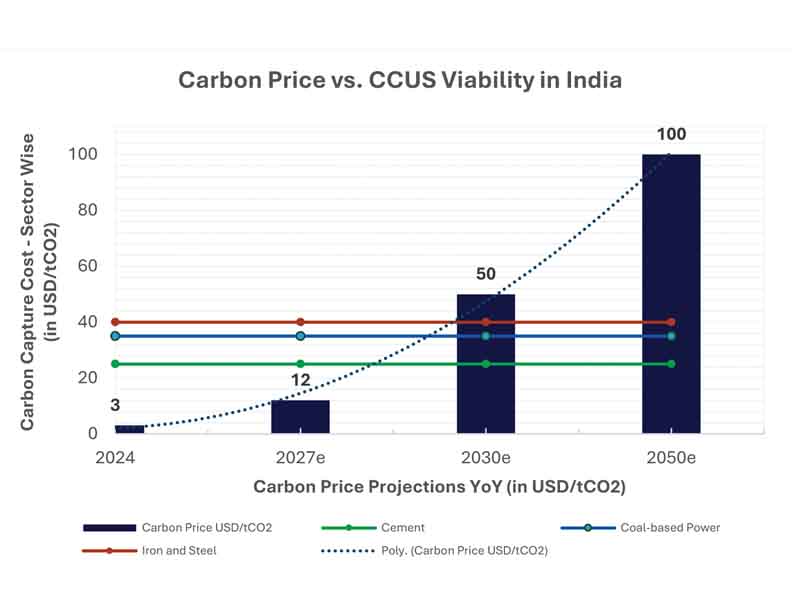

Currently, the approximate carbon capture itself costs ~70% of the overall CCUS cost and ranges from ~`1800 to `3500 per tonne (US$20–40/tCO2) depending upon industrial sector (shown in chart) as per the study conducted by NITI Ayog on CCUS deployment in India. The economics are clear, when emitting costs exceed capture, CCUS becomes a profitable compliance tool. As the carbon prices approach `4000 per tonne ($45-50/tCO2) and above, carbon capture becomes economically viable and cost-competitive for India’s heavy industry.

Carbon Pricing as the Trigger: India’s CCUS becomes viable when carbon prices hit $40–50/tCO2, scalable above $70, and profitable for utilisation at and beyond $100/tCO2 under compliance markets.

Monetisation Models – Turning Capture into Commerce

Currently, most CCUS pilot projects in India are centered on technology validation. The next step is to develop revenue models that support the economic sustainability of capture. The question is no longer – can we capture CO2, but how can we make it pay?

How do Business Models Enable Monetisation?

Carbon capture typically accounts for ~70% of total CCUS costs, making it the most capital-intensive stage. The key to monetisation lies in transforming capture into a service-based or product-linked offering that aligns financial returns with emission reductions.

Capture-as-a-Service, Storage-as-a-Service, and Merchant CO2 Hubs are examples of emerging CCUS business models that aim to generate recurring revenue, attract private investment, and support the development of a carbon market ecosystem. Based on global case studies, establishing carbon pricing and transparent Measurement, Reporting, and Verification (MRV) frameworks in India would be a key factor in supporting the financial feasibility of capture and storage. Additionally, demand creation through green-product procurement and the establishment of regional CCUS hubs may contribute to developing a scalable industrial ecosystem for carbon management. CCUS is more profitable when offered as a service or product instead of just for compliance.

The Road Ahead – Building India’s Carbon Economy

To evolve from pilots to a nationwide carbon management industry, India must make three strategic shifts:

- From Project to Service: Treat capture and storage as pay-per-use utilities (CaaS, SaaS).

- From Subsidy to Market: Build robust carbon trading ecosystems to sustain long-term revenues.

- From Silos Pilots to Clusters: Develop regional CCUS hubs in Gujarat, Odisha, and Tamil Nadu to pool emitters, pipelines, and storage.

Carbon monetisation is the missing bridge between ambition and action. As carbon markets mature, CCUS will shift from policy experiment to industrial norm. By 2030, India could anchor Asia’s first carbon management economy, linking heavy industry with green innovation and new revenue streams.

Payal Saxena has 9 years of experience in Renewable Energy, Energy Transition and Utilities. She has worked extensively with Global Utilities, IPPs, and Industries on developing Renewable and Decarbonisation strategies, policy advocacy initiatives, techno-economic analysis, business and operating models, to facilitate a low carbon economy, systemic efficiency, and net zero transition.